Trending News:This is how Abhishek Sharma’s upset stomach endedHebron under Israeli blockade in wider West Bank annexation plan Israeli-Palestinian conflictValentine’s Day Relationship Advice: How to Overcome ConflictPing! WhatsApp messages should be an email6 lucrative jobs from homeEngland take two quick wickets against West Indies in T20 World CupFans erupt as Nathan Ellis and Adam Zampa beat Ireland to help Australia register emphatic win at T20 World Cup 2026Norwegian Olympian’s ex speaks out after personal life leaksLevl raises $7 million to provide stablecoin infrastructure for fintechsCriteo shares fall after quarterly earnings miss7 Weird Space Oddities That Only Make Sense If Dark Matter ExistsChelsea offer to sign Marco Senesi in AFC Bournemouth future updateJanuary 2026 Employment Report:Iran celebrates its revolution, and American warships lurk off the coastJanuary 2026 jobs report: US economy added 130,000 jobs amid solid growthKeefe, Bruyette & Woods lowered its price target on Zillow stock to $60 from $65How to Set Up Apple Watch for Your Kids (2026)T20 World Cup: India vs NamibiaWWE News Roundup – Female Stars Leaving Company; Bron Breakker Missed from WrestleMania 42; The Real Reasons Judgment Day Members Missed RAWWhat are the gun ownership laws in Canada?US Attorney Bondi will face questions about the Epstein files in House testimonyGovt to transfer Rs 25.44 lakh crore to states in FY27 through tax refund: FM SitharamanIND vs NAM Match 18 Preview: Free Live Stream, Pitch & Weather Report, Head to Head, Match LineupClient ChallengeT20 World Cup, England vs West Indies Live! Latest scores, updates and highlights as Harry Brook’s side chase Group C victory | Cricket NewsAre drones and artificial intelligence making it more difficult to attack armed groups in the Sahel? |Armed Group NewsA Ukrainian father and his three small children were killed in an attack by a Russian drone, and a pregnant mother was seriously wounded.What drives record CFO turnover?Snap-On’s price target rose to $409 from $385 at Roth CapitalT20 World Cup 2026: Paul Sterling withdraws injured in crucial match against Australia, dealing blow to IrelandNottingham Forest hires “genius” 4-2-3-1 Dyche for freeBrain health experts say the hardest time of day to consume sugar may surprise you9 killed and 25 wounded in shooting at Tumbler Ridge, CanadaNeedham lowered his price target on Cloudflare stock to $250 on the growth outlookEarnings Snapshot: Shopify Beats Q4 Revenue Estimates; begins the outlook for the first quarterWhat went wrong at Tottenham and what should happen nowNFL analysts mock right-wingers after ‘Bad Bunny’ halftime show breaks record by averaging 128.2 million viewersKraft Heinz pauses efforts to break up company, says challenges ‘can be solved’Yossi Mekelberg warns of Israel’s current measures aimed at ‘killing’ peace and the two-state solutionClient Challenge‘Issuing executive orders gives Trump a sense of power’: Kanwal Sibal on US-India-Russia dynamicsParamount wants out of ‘Teenage Mutant Ninja Turtles’Tilak Varma provides key update on Abhishek Sharma ahead of conflict in NamibiaThomas Frank sacked by Tottenham after eight months in charge: What went wrong with the former Brentford boss? |Football NewsBBC celebrates 47th anniversary of Iran’s Islamic Revolution in TehranPowell’s parting gift from the Fed may be more rate cuts than expectedPolicy changes and sales fluctuations continue to affect the Chinese marketRazer Huntsman V3 Pro 8KHz Review: A Keyboard for the CompetitiveDelhi Capitals hire England legend as assistant coach ahead of IPL 2026Arsenal in pole position to sign Christian PulisicTottenham Hotspur manager Thomas Frank sacked after eight months Football NewsNATO is expected to strengthen security in the Arctic. Here’s why.Form 13G Perceptive Capital Solutions Corp Due: 11 FebruaryKraft Heinz on the charts: Q4 North American sales fall 5.4%, mark 10th consecutive y/y decline; international sales increaseConnor Benn says super middleweight would have beaten his dad in his prime: ‘I’m sorry’ONE Fight Night 40: “Total Lockdown”WWE legend says his gallbladder ‘exploded’Suspect arrested in kidnapping of Nancy Guthrie after video released of armed manClient ChallengeIND vs PAK T20 World Cup: Colombo flight fares have reached over ₹1 lakh from THESE cities. Details hereThe 2027 Toyota Highlander is fully electric and has a 320-mile rangeThe Barcelona forward will miss the Copa clashU.S. state tariff bills hit $200 billionLaw enforcement thought Nancy Guthrie’s smart camera had been hacked, but Google Nest still had the tapeFactbox-EU Tariffs on Electric Vehicle Imports Made in ChinaHow can Afghanistan, which has suffered back-to-back defeats in the 2026 T20 World Cup, still advance to the Super 8?Dawson backs Keane to take over as Tottenham manager!Best Speakers of 2026 – CNETGhana declares Wednesday ‘Puffer Day’ to promote traditional clothing after online ridiculeThe revelations in Epstein’s files led to resignations and investigations around the worldForm 13D/A Niu Technologies Due: 11 FebruaryNon-GAAP EPS of TotalEnergies SE of €1.48AUS vs IRE (WATCH): Spinner Matthew Humphreys’ 110km/h lightning blast destroys Matt Renshaw’s mid-stump | T20 World Cup 202649ers consider selling ‘outstanding’ Rangers star on £20,000-a-week deal this summerMike Flanagan Has His Next Stephen King Adaptation: ‘The Mist’Russian drone kills father, 3 children, injures pregnant mother in Ukraine Russia-Ukraine war newsCanada’s stricter immigration policy is dividing the countryClient ChallengeEl Paso airport closed for 10 days for ‘special security reasons’David Benavidez says there’s a man who surpassed Crawford as the best player of this eraHow to Defeat All Cyberstan Cyborgs in Helldivers 2Wacom MovinkPad 11 Tablet Review: A Portable Sketch PadLawmakers shocked after Democratic police chief couldn’t answer basic ‘fifth grade’ citizen questionsA decade after his kneeling NFL controversy, Colin Kaepernick has a message for Gen ZAdditional travel included: Malaysia Airlines offers advance fares to IndiaNevada Rep. Titus opens prediction markets bill targeting sports loopholes oversight pushDanish Kaneria rips Pakistan cricket and government apart after shocking U-turn on boycott decisionChampionship play-offs: EFL likely to select six-team expanded format ahead of 2026/27 AGM | Football NewsTotalEnergies explains why it won’t support Trump’s Venezuela dreamAmazon Pharmacy to expand same-day delivery to nearly 4,500 US cities and towns‘I will meet every victim,’ says the mayor of close-knit Tumbler Ridge.The best CD rates today, February 11, 2026 (Earn up to 4% APY)The DOJ could face an investigation into the removal of ICE agent tracking appsAUS vs IRE, T20 World Cup 2026: Here’s why Mitchell Marsh won’t play today‘Outstanding’ 4-2-3-1 coach could become Spurs’ new managerAustralia’s opposition leader under pressure after key resignationGoogle AI boss Demis Hassabis has a 4-step plan to bring the tech giant back to its ‘golden age’The Nancy Guthrie case was ‘opened up’ by the camera footage of the doorbellVertiv misses Q4 street estimates, guides Q1 FY numbersToday’s NYT Wordle Hints, Answers and Help for Feb. 11 #1698

Trending News:This is how Abhishek Sharma’s upset stomach endedHebron under Israeli blockade in wider West Bank annexation plan Israeli-Palestinian conflictValentine’s Day Relationship Advice: How to Overcome ConflictPing! WhatsApp messages should be an email6 lucrative jobs from homeEngland take two quick wickets against West Indies in T20 World CupFans erupt as Nathan Ellis and Adam Zampa beat Ireland to help Australia register emphatic win at T20 World Cup 2026Norwegian Olympian’s ex speaks out after personal life leaksLevl raises $7 million to provide stablecoin infrastructure for fintechsCriteo shares fall after quarterly earnings miss7 Weird Space Oddities That Only Make Sense If Dark Matter ExistsChelsea offer to sign Marco Senesi in AFC Bournemouth future updateJanuary 2026 Employment Report:Iran celebrates its revolution, and American warships lurk off the coastJanuary 2026 jobs report: US economy added 130,000 jobs amid solid growthKeefe, Bruyette & Woods lowered its price target on Zillow stock to $60 from $65How to Set Up Apple Watch for Your Kids (2026)T20 World Cup: India vs NamibiaWWE News Roundup – Female Stars Leaving Company; Bron Breakker Missed from WrestleMania 42; The Real Reasons Judgment Day Members Missed RAWWhat are the gun ownership laws in Canada?US Attorney Bondi will face questions about the Epstein files in House testimonyGovt to transfer Rs 25.44 lakh crore to states in FY27 through tax refund: FM SitharamanIND vs NAM Match 18 Preview: Free Live Stream, Pitch & Weather Report, Head to Head, Match LineupClient ChallengeT20 World Cup, England vs West Indies Live! Latest scores, updates and highlights as Harry Brook’s side chase Group C victory | Cricket NewsAre drones and artificial intelligence making it more difficult to attack armed groups in the Sahel? |Armed Group NewsA Ukrainian father and his three small children were killed in an attack by a Russian drone, and a pregnant mother was seriously wounded.What drives record CFO turnover?Snap-On’s price target rose to $409 from $385 at Roth CapitalT20 World Cup 2026: Paul Sterling withdraws injured in crucial match against Australia, dealing blow to IrelandNottingham Forest hires “genius” 4-2-3-1 Dyche for freeBrain health experts say the hardest time of day to consume sugar may surprise you9 killed and 25 wounded in shooting at Tumbler Ridge, CanadaNeedham lowered his price target on Cloudflare stock to $250 on the growth outlookEarnings Snapshot: Shopify Beats Q4 Revenue Estimates; begins the outlook for the first quarterWhat went wrong at Tottenham and what should happen nowNFL analysts mock right-wingers after ‘Bad Bunny’ halftime show breaks record by averaging 128.2 million viewersKraft Heinz pauses efforts to break up company, says challenges ‘can be solved’Yossi Mekelberg warns of Israel’s current measures aimed at ‘killing’ peace and the two-state solutionClient Challenge‘Issuing executive orders gives Trump a sense of power’: Kanwal Sibal on US-India-Russia dynamicsParamount wants out of ‘Teenage Mutant Ninja Turtles’Tilak Varma provides key update on Abhishek Sharma ahead of conflict in NamibiaThomas Frank sacked by Tottenham after eight months in charge: What went wrong with the former Brentford boss? |Football NewsBBC celebrates 47th anniversary of Iran’s Islamic Revolution in TehranPowell’s parting gift from the Fed may be more rate cuts than expectedPolicy changes and sales fluctuations continue to affect the Chinese marketRazer Huntsman V3 Pro 8KHz Review: A Keyboard for the CompetitiveDelhi Capitals hire England legend as assistant coach ahead of IPL 2026Arsenal in pole position to sign Christian PulisicTottenham Hotspur manager Thomas Frank sacked after eight months Football NewsNATO is expected to strengthen security in the Arctic. Here’s why.Form 13G Perceptive Capital Solutions Corp Due: 11 FebruaryKraft Heinz on the charts: Q4 North American sales fall 5.4%, mark 10th consecutive y/y decline; international sales increaseConnor Benn says super middleweight would have beaten his dad in his prime: ‘I’m sorry’ONE Fight Night 40: “Total Lockdown”WWE legend says his gallbladder ‘exploded’Suspect arrested in kidnapping of Nancy Guthrie after video released of armed manClient ChallengeIND vs PAK T20 World Cup: Colombo flight fares have reached over ₹1 lakh from THESE cities. Details hereThe 2027 Toyota Highlander is fully electric and has a 320-mile rangeThe Barcelona forward will miss the Copa clashU.S. state tariff bills hit $200 billionLaw enforcement thought Nancy Guthrie’s smart camera had been hacked, but Google Nest still had the tapeFactbox-EU Tariffs on Electric Vehicle Imports Made in ChinaHow can Afghanistan, which has suffered back-to-back defeats in the 2026 T20 World Cup, still advance to the Super 8?Dawson backs Keane to take over as Tottenham manager!Best Speakers of 2026 – CNETGhana declares Wednesday ‘Puffer Day’ to promote traditional clothing after online ridiculeThe revelations in Epstein’s files led to resignations and investigations around the worldForm 13D/A Niu Technologies Due: 11 FebruaryNon-GAAP EPS of TotalEnergies SE of €1.48AUS vs IRE (WATCH): Spinner Matthew Humphreys’ 110km/h lightning blast destroys Matt Renshaw’s mid-stump | T20 World Cup 202649ers consider selling ‘outstanding’ Rangers star on £20,000-a-week deal this summerMike Flanagan Has His Next Stephen King Adaptation: ‘The Mist’Russian drone kills father, 3 children, injures pregnant mother in Ukraine Russia-Ukraine war newsCanada’s stricter immigration policy is dividing the countryClient ChallengeEl Paso airport closed for 10 days for ‘special security reasons’David Benavidez says there’s a man who surpassed Crawford as the best player of this eraHow to Defeat All Cyberstan Cyborgs in Helldivers 2Wacom MovinkPad 11 Tablet Review: A Portable Sketch PadLawmakers shocked after Democratic police chief couldn’t answer basic ‘fifth grade’ citizen questionsA decade after his kneeling NFL controversy, Colin Kaepernick has a message for Gen ZAdditional travel included: Malaysia Airlines offers advance fares to IndiaNevada Rep. Titus opens prediction markets bill targeting sports loopholes oversight pushDanish Kaneria rips Pakistan cricket and government apart after shocking U-turn on boycott decisionChampionship play-offs: EFL likely to select six-team expanded format ahead of 2026/27 AGM | Football NewsTotalEnergies explains why it won’t support Trump’s Venezuela dreamAmazon Pharmacy to expand same-day delivery to nearly 4,500 US cities and towns‘I will meet every victim,’ says the mayor of close-knit Tumbler Ridge.The best CD rates today, February 11, 2026 (Earn up to 4% APY)The DOJ could face an investigation into the removal of ICE agent tracking appsAUS vs IRE, T20 World Cup 2026: Here’s why Mitchell Marsh won’t play today‘Outstanding’ 4-2-3-1 coach could become Spurs’ new managerAustralia’s opposition leader under pressure after key resignationGoogle AI boss Demis Hassabis has a 4-step plan to bring the tech giant back to its ‘golden age’The Nancy Guthrie case was ‘opened up’ by the camera footage of the doorbellVertiv misses Q4 street estimates, guides Q1 FY numbersToday’s NYT Wordle Hints, Answers and Help for Feb. 11 #1698

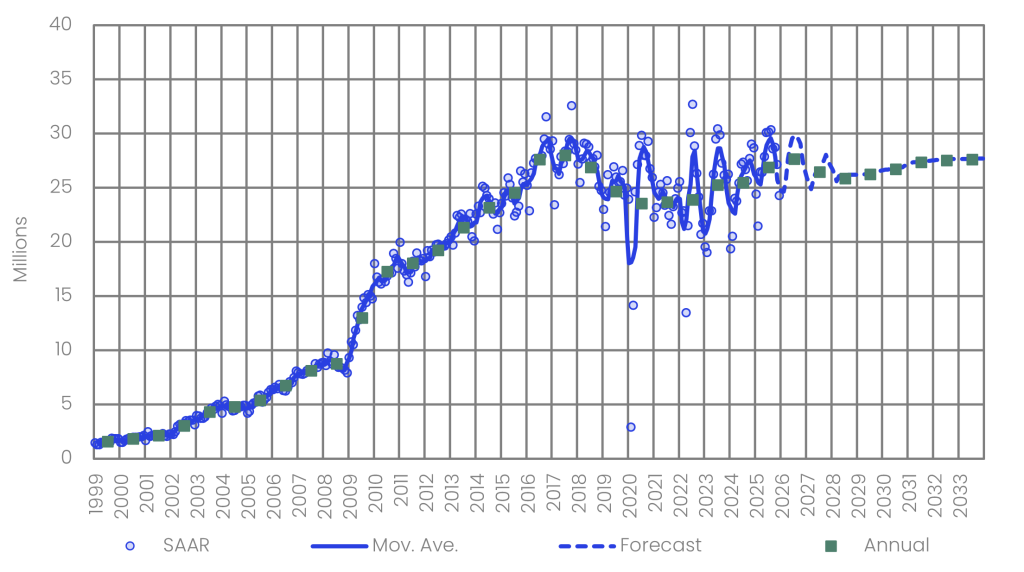

With subsidies suspended in a wide range of regions, light vehicle (LV) sales in China posted negative growth in December. Total volumes reached approximately 2.5 million units, representing a 16% year-over-year (YoY) decline. The passenger vehicle (PV) segment, which fell 17% year-on-year to 2.2 million units, remained the main driver, while the light commercial vehicle (LCV) segment posted a modest 1% year-on-year increase to 240,000 units. For the full year 2025, LVs still performed well, with total volumes reaching 26.9 million units, up 6% year-on-year. Similarly, by segment, both PV and LCV grew by 6% year-on-year. The seasonally adjusted annualized sales rate (SAAR) for December was 24.2 million units, down 15% compared to the same period in 2024.

Source: GlobalData

During the month, China’s BT production totaled 3.1 million units (-3.5% y-o-y). PV production, which accounted for 90% of the total, fell 4.1% year-on-year to 2.9 million units, but still pointed to sustained consumer demand and market resistance. In contrast, CV production increased by 2.5% year-on-year to 291,000 units. Chinese domestic OEMs posted their first production decline, down 0.4% year-on-year to 2.3 million units, while joint-venture OEMs remained under pressure, with production down 11.1% year-on-year. On the other hand, exports were a clear bright spot. During the month, China shipped 684,000 LVs, which represented strong growth of 47.5% y-o-y and 3.0% month-on-month (MoM), driven mainly by PVs, as overseas deliveries rose 48.1% y-o-y to 633,000 units. CV exports also strengthened, rising 42.4% year-on-year to 72,000 units. For the whole year 2025, total LV exports reached 6.6 million units, a year-on-year expansion of 19.4%.

Overall, China’s auto market slowed sharply in December, with momentum quickly cooling — effectively a “quick freeze” — as a combination of factors weighed on demand. The usual year-end sales surge, known as the “tail effect”, did not materialize, likely because many consumers brought forward their purchases in line with the “golden September and silver October” sales season and to take advantage of regional “exchange” subsidies. Thus, sales between January and October increased by 7% year-on-year, well above the typical levels of recent years. In addition, as of November, grant budgets were depleted in many regions, leading to application suspensions that reduced the expected policy increase and softened replacement demand. Adding to the hesitation, from 2026, the tax on the purchase of new energy vehicles (NEV) will go from full exemption to a 50% reduction; however, implementation details have been delayed, causing many consumers to postpone their purchases and further widening the year-end demand gap.

December’s decline thus reflected the combined effects of fading policy support, consumer hesitancy, ongoing industry transformation, particularly the shift from gasoline vehicles to NEVs, and inventory pressures. This suggests that the market is entering a new phase of deeper adjustment and restructuring, going beyond the era of rapid growth.

Looking to 2025, China’s automobile industry delivered solid progress in scale, structural optimization, technological innovation and market standardization, indicating a shift to a new phase of high-quality development. Both LV production and sales reached record highs. NEV sales exceeded 13 million units, up 20% year-on-year, and became the main growth force in the market. To address “rollover-style” competition, regulators introduced a number of measures during the year, including measures to curb disorderly price wars, encouraging automakers to honor payment commitments, running targeted campaigns to address online disorder, and issuing guidelines on price compliance practices, all aimed at maintaining healthy competitive conditions. At the same time, the regulatory and security framework has continued to improve. The Ministry of Industry and Information Technology made the requirement of “no fire, no explosion” mandatory for power batteries, standardized hidden door handles, and put pure electric photovoltaics under export license management. Supervision of used car exports was also strengthened to support the sustainable development of the industry.

In 2026, China’s auto market will likely enter a crucial stage, moving from “scale competition” to “capacity competition”. From a policy perspective, adjustments to the NEV purchase tax, an updated trade-in subsidy program, and a stricter dual credit policy will directly affect consumers’ vehicle purchase costs and automakers’ strategic priorities. In general, the policy focus is shifting from broad-based stimulus to more targeted support, an approach that should be more sustainable in the long term. Two features stand out. First, linking subsidies to new vehicle prices should help prevent the previous practice of “profiteering” through low-priced models and ensure that tax resources are more precisely targeted at improving consumer demand. Second, prior clarification of policy details should stabilize consumer expectations and reduce irrational spikes in last-minute purchases seen in previous years before grant deadlines. Based on current conditions, we expect the domestic market in 2026 to increase slightly or remain flat from 2025, while exports should maintain double-digit expansion. NEVs, foreign markets and downstream markets will remain the key pillars of growth. At the same time, the transformation of the sector is likely to accelerate even further, intensifying consolidation and accelerating the cycle of “survival of the fittest”.

Source: GlobalData

“Policy changes and sales fluctuations continue to affect China market” was originally created and published by Automatic onlya trademark owned by GlobalData.

The information on this site has been included in good faith for general informational purposes only. It is not intended to be advice on which you should rely, and we make no representations, warranties or guarantees, either express or implied, as to its accuracy or completeness. You should obtain professional or specialist advice before taking or refraining from any action based on the content of our site.

Am I the only one using email instead of WhatsApp? Maybe so. I’m having a harder time persuading my contacts – and more frighteningly, my friends – to use email…

As someone who has been working from home for nine years, I can say without reservation that I love my office. It’s conveniently located just a few steps from my…